The market story everyone got wrong in January 2026 was simple: rate cuts were coming, risk assets would rip, and Bitcoin would print new highs. Five months later, the script has flipped. Traders are now pricing in a Fed rate hike instead of a cut, Bitcoin is hovering near $75,000 after a brutal slide, and “Extreme Fear” is back on the dashboard.

If you invest in stocks, crypto, or anything that breathes when liquidity expands, this is the regime shift that matters most right now. Here’s what changed, why it’s hitting every asset class at once, and how disciplined investors are positioning into the back half of 2026.

The Fed Just Changed Captains — and Direction

The biggest macro headline of the spring wasn’t a data point. It was a personnel change. Kevin Warsh was sworn in as Federal Reserve chair in late May, replacing Jerome Powell, whose term expired on May 15. New chair, new tone.

Here’s the kicker: bond traders are betting Warsh’s first move will be to raise rates, not lower them. According to the CME FedWatch Tool, markets are now pricing roughly a 70% chance of a rate hike before year-end, with the heaviest odds on a single quarter-point increase from the current 3.50%–3.75% target range. That is a near-total reversal of the easing narrative that dominated late 2025.

For context, the Fed had already cut 175 basis points since September 2024. The expectation heading into 2026 was “one or two more cuts.” Instead, persistent inflation flipped the table. Bank of America pushed its rate-cut forecast all the way out to mid-2027, and even JPMorgan’s Jamie Dimon floated a blunt warning about an eventual credit recession being worse than the market expects.

Why the U-turn? One word: oil

The inflation that refuses to die is being fed by an energy shock. The ongoing Iran war pushed crude sharply higher — WTI traded around $104 — and energy prices feed straight into headline CPI, which has been running well above the Fed’s 2% target (recent reads in the 3.3%–3.7% zone). A central bank can’t credibly cut into a fresh inflation impulse, so “higher for longer” hardened into “maybe higher, period.”

There is a glimmer on the geopolitical side: reports point to a potential U.S.–Iran draft agreement, with the Strait of Hormuz possibly reopening to shipping within 30 days. If that holds, oil could cool — and the entire rate calculus softens with it. Watch the oil tape; it’s the real Fed input right now.

Crypto Is Taking the Macro Punch

When real yields rise and liquidity tightens, the most speculative assets get repriced first. Crypto is doing exactly that.

Bitcoin has been grinding lower, trading in the $74,000–$76,000 band after a multi-day losing streak — a long way from its earlier-year ambitions. Ethereum slipped to around $2,081, and total crypto market capitalization compressed to roughly $2.62 trillion. The Crypto Fear & Greed Index dropped into “Extreme Fear” near 25, its lowest in weeks.

The flows tell the cleanest story. The crypto market posted its worst weekly ETP outflow of 2026 at about $1.47 billion. In plain terms: institutional money walked out the door before retail sentiment even caught up. Exits ran ahead of fear, not behind it.

It wasn’t only macro. A high-profile holder unwinding a large Ethereum position and chatter about restrictions on a major retail on-ramp added selling pressure on top of the rate story. None of it is a “crypto is broken” signal — it’s a liquidity-and-positioning signal.

The contrarian read

Extreme Fear and capitulation-style outflows are the conditions long-term allocators historically watch for, not the ones they run from. That doesn’t mean the bottom is in — it means the risk/reward starts shifting for those with a multi-year horizon and the stomach for volatility. Capitulation is uncomfortable by design.

The Quiet Bull Case Hiding Under the Red Tape

Strip away the daily candles and 2026 has produced some of the most important structural wins crypto has ever had. These are the stories that compound long after the rate cycle resolves.

Stablecoins went truly mainstream. Cash App began rolling out USDC transfers to roughly 60 million users across Solana, Ethereum, Polygon, and Arbitrum — with zero fees and instant conversion to dollars. When a mass-market consumer app puts on-chain dollars in tens of millions of pockets, the addressable market changes permanently.

Regulation got a real framework. A new digital commodity taxonomy from the SEC and CFTC moved from guidance into its first practical applications in May. Clear rules of the road are exactly what large allocators have been waiting for before sizing up.

Tokenization is no longer a buzzword. Tokenized stock trading volume hit a record of about $3.57 billion in a single day, and prediction markets pushed into private-company valuations. The line between “crypto” and “capital markets” is blurring fast.

The takeaway: price is in a drawdown, but adoption is on a tear. Those two things rarely stay disconnected forever.

What About Stocks?

Equities have been more resilient than crypto, and the reason is earnings. Strong first-quarter results powered stocks even as bond yields climbed and the Iran conflict stayed unresolved. Solid corporate profits, resilient consumer spending, and heavy technology investment are doing the heavy lifting.

The caution flag: analysts at Morningstar noted that AI and growth stocks no longer offer much of a margin of safety after their run, and market concentration keeps climbing. Higher-for-longer rates also make bonds a genuine competitor for capital — when short-term Treasuries pay well, investors get pickier about what multiple they’ll pay for future growth.

The 2026 Investor Playbook

This isn’t financial advice — it’s a framework for thinking through a higher-rate, higher-uncertainty tape. Here’s how disciplined investors are approaching it:

Respect the rate regime. If the next Fed move is a hike, the “buy every dip in speculative assets” reflex from the easy-money era is the wrong default. Position sizing matters more than conviction.

Watch oil as your inflation tell. A genuine Iran de-escalation that cools crude could re-open the door to cuts — and re-rate risk assets quickly. The geopolitical headline is the macro trade.

Separate price from adoption in crypto. Drawdowns are loud; structural wins (stablecoins, clear regulation, tokenization) are quiet but durable. Build your thesis on the second, not the first.

Don’t ignore the income on offer. With short rates near 3.5%–3.75%, cash and short-duration bonds finally pay you to wait. Patience has a yield again.

Mind concentration. Mega-cap AI names carry the indexes; understand how much of your portfolio is really one trade in disguise.

FAQ

Is the Fed actually going to raise rates in 2026? Nothing is guaranteed, but as of late May 2026 markets priced roughly a 70% chance of at least one hike before year-end, with new chair Kevin Warsh widely expected to lean hawkish. The path depends heavily on oil prices and inflation data.

Why is Bitcoin falling if crypto adoption is growing? Price reflects short-term liquidity and positioning; adoption reflects long-term demand. In 2026, tightening Fed expectations and large institutional outflows pushed prices down even as real-world usage (like Cash App’s USDC rollout) expanded.

Is now a good time to buy the dip? That depends entirely on your time horizon, risk tolerance, and goals. “Extreme Fear” historically marks zones long-term investors study closely, but it is not a guarantee of a bottom. This article is educational, not personalized advice.

What’s the single biggest variable to watch? Oil. The Iran war is the main inflation driver keeping the Fed hawkish. A credible peace deal that reopens the Strait of Hormuz could cool inflation and reset the entire rate outlook.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. Cryptocurrency and equity markets are volatile and you can lose money. Always do your own research and consider speaking with a licensed financial professional before making investment decisions.

Tuesday morning, the CPI report landed and made headlines everywhere.

Inflation at 3.8%. Highest since May 2023. Gasoline up 28.4% over the year. Beef up 14.8%. Airline fares up 20.7%. Real wages falling for the second consecutive month. Rate hike odds climbing to 30%.

It was alarming enough that markets sold off. It was alarming enough that Moody’s chief economist Mark Zandi said American households are “going to continue to struggle trying to manage through this, and that’s going to be the case for the foreseeable future.” It was alarming enough that CME futures traders are now pricing zero probability of any rate cuts in 2026.

Then Wednesday morning, the Producer Price Index dropped.

And it was three times worse than expected.

PPI rose 1.4% in a single month — against a Wall Street consensus forecast of 0.5%. Three times the estimate. The largest monthly gain since March 2022. On an annual basis, producer prices are up 6.0% — the biggest increase since December 2022. Core PPI, which strips out food and energy, rose 1.0% for the month — 2.5 times the 0.4% estimate.

After the PPI, rate hike odds jumped from 30% to 39%.

Here is why both numbers matter, why most people are only reading one of them, and why the combination of Tuesday’s CPI and Wednesday’s PPI is the most important inflation signal of 2026 — telling you not just where prices are today, but where they are going in the next 30 to 90 days.

The Difference Between CPI and PPI That Changes Everything

Most people have heard of CPI. Most people have not heard of PPI. That asymmetry is one of the most expensive information gaps in personal finance.

CPI — the Consumer Price Index — measures what you pay. It is the number that shows up in headlines, that politicians cite, that the Fed’s 2% target refers to. It captures prices at the point of final sale: the gallon of gas at the pump, the package of beef at the grocery store, the airline ticket on the booking website.

PPI — the Producer Price Index — measures what businesses pay. It captures prices at earlier stages of the supply chain: what manufacturers pay for raw materials and components, what wholesalers pay to distributors, what service firms pay for their inputs. It is the upstream number. The number that flows downstream into consumer prices with a lag.

The lag matters. Economists who study price transmission consistently find that changes in the PPI lead changes in the CPI by approximately 30 to 90 days. When producer prices spike, consumer prices follow — not immediately, but predictably, as businesses pass their higher input costs through to retail prices over the subsequent weeks and months.

This means Tuesday’s 3.8% CPI is a measurement of where prices were in April. Wednesday’s 6.0% PPI is a measurement of where prices are going between now and July.

Tuesday told you what happened. Wednesday told you what is coming.

The Number That Should Be Making Every Headline

Producer prices up 6.0% annually. 1.4% in a single month. The core reading — excluding food and energy, revealing underlying structural inflation — up 1.0% in a single month, 2.5 times the estimate.

Let those numbers sit alongside each other for a moment.

The Fed’s inflation target is 2% annually. Producer price inflation is running at 6% annually — three times the target — at the wholesale level, before it flows through to consumers. Core producer prices, which are supposed to be the more stable, structural measure of underlying inflation, rose 1.0% in a single month. Annualized, that is 12% core PPI inflation.

“Inflation is sticky and accelerating. The core reading confirms a deeper structural trend, especially in services,” said David Russell, global head of market strategy at TradeStation. “The Hormuz crisis is aggravating the problem, but this goes way beyond oil.”

That last sentence is the most important thing said about inflation this week.

The PPI report shows that the price pressures were broad-based. The services index accelerated 1.2%, the biggest monthly gain since March 2022. Two-thirds of the services move was attributed to a 2.7% rise in trade services — a sign that tariff costs are starting to have a larger impact on prices beyond the direct impact on goods. The move was also buttressed by a 3.5% jump in margins for machinery and equipment wholesaling.

This is not an oil story. Oil explains the energy component. Oil explains gasoline at $4.50 nationally. Oil explains jet fuel costs driving airline fares up 20.7% annually.

But services inflation at 1.2% monthly is not an oil story. Trade services inflation at 2.7% monthly is not an oil story. Machinery and equipment wholesaling margins up 3.5% is not an oil story.

These are structural inflation pressures — the kind that the Fed’s rate hiking cycle of 2022-2023 was supposed to have defeated. They are re-accelerating in 2026, driven partly by the Iran war and partly by tariff pass-through that is now moving through supply chains with enough lag that it is showing up in April data from tariffs announced months earlier.

The “Double Squeeze” Hitting Every American Household

Before the CPI and PPI data, a Bankrate analyst described what consumers are experiencing as a “double squeeze” — wrestling with both the acute pain of the gasoline price spike and the slow rise in other core budget items. The data from this week confirms and quantifies that description.

The acute pain — energy:

Gasoline prices are up 28.4% over the past twelve months. The national average is now $4.50 per gallon. In California, prices are above $5. Energy overall is up 17.9% annually — the steepest increase since September 2022. Fuel oil is up 54.3% annually.

These numbers represent a direct, unavoidable tax on every American who drives a car, heats a home with oil, or flies. They show up immediately in household budgets and cannot be managed with behavioral changes beyond the margins — most Americans cannot stop commuting, cannot stop heating their homes, cannot stop flying for essential travel.

The slow burn — everything else:

Food at home prices rose 0.7% in April alone — the biggest monthly gain since August 2022. Beef is up 14.8% over the year. Food overall is up 3.2% annually.

Shelter costs rose 0.6% in April — and this is where the report contains the most alarming signal for the inflation outlook. Shelter inflation had been decelerating in prior months. In April, it reaccelerated. Shelter is the single largest component of the CPI basket — it represents approximately 34% of the total index. When shelter inflation is decelerating, it pulls the overall number down. When it reaccelerates, as it did in April, it adds a persistent, sticky component that is extremely difficult to reverse quickly.

Airline fares rose 2.8% in a single month — putting the twelve-month gain at 20.7%. This is the direct pass-through of jet fuel costs, and it affects every American who travels for work, family events, or vacation. The consumer who budgeted their summer trip in January is now looking at ticket prices that are 20% higher than they were a year ago.

Apparel was up 0.6% for the month — the tariff effect flowing through clothing supply chains. Household furnishings and operations were up 0.7% — the tariff effect flowing through the furniture and home goods supply chains that depend heavily on Asian imports.

The “double squeeze” is not two separate problems. It is one problem — an inflation shock with both an acute energy component and a persistent, broadening structural component — expressing itself across nearly every category of household spending simultaneously.

39 Percent. That Is the Number That Changes Everything.

Before Tuesday’s CPI, markets were pricing a 25% probability of a Fed rate hike in 2026.

After Tuesday’s CPI, that probability rose to approximately 30%.

After Wednesday’s PPI — with its 1.4% monthly surge and 6.0% annual rate — that probability jumped to 39%.

39% probability of a rate hike.

This is the number that has not existed in serious market pricing for years. Since 2023, the debate has been entirely about when the Fed would cut rates, not whether it might raise them. The entire investment thesis of 2024 and early 2025 — own long-duration bonds, own growth stocks, own real estate — was built on the assumption that rate cuts were a matter of timing, not direction.

Wednesday’s PPI has placed serious institutional money on the possibility that the next Fed move is not a cut but a hike.

If the Fed raises rates from the current 3.5-3.75% range — in an economy where consumer confidence is at a 75-year low, the household survey is showing employment declines, and residential construction is contracting — the consequences are not theoretical. They are specific and painful.

Mortgage rates, already at 6.75-7%, would move toward 7.25-7.5%. Monthly payments on a $400,000 mortgage would increase by $150-200. The housing market, already struggling, would face further demand destruction.

Credit card rates, already at 22-24%, would increase further. The record $1.277 trillion in American credit card balances would generate more interest income for the banks and more payment burden for the families carrying those balances.

Business borrowing costs would rise. Companies with variable-rate debt — the most common structure for small and medium-sized businesses — would see their interest expenses increase immediately. Businesses operating on thin margins in sectors already squeezed by input cost inflation would face the additional pressure of higher financing costs.

39% is not a certainty. It is not even a majority position. But it is a serious institutional assessment that the inflation data of this week has moved the probability of a rate hike from theoretical to plausible. And plausible, in financial markets, moves asset prices.

What the PPI Says About June’s CPI

The 30-90 day transmission lag between PPI and CPI is well-documented in economic research. Using the April PPI data, it is possible to make a directional forecast about where CPI will be when the June 10 report covers May prices.

The PPI signals suggest that May and June CPI will face continued upside pressure from at least three channels.

Energy pass-through: The 1.4% monthly PPI gain was led by energy. That energy cost increase at the producer level has not yet fully passed through to retail prices. Gas station prices respond quickly, but utility bills, transportation costs, and the embedded energy cost in food production and distribution respond more slowly. The full energy pass-through from April’s PPI will still be flowing into May retail prices when the June 10 CPI report is released.

Services inflation persistence: The 1.2% monthly gain in services PPI — driven by trade services and warehousing — takes longer to transmit to consumer prices than goods inflation, but it is more persistent once it arrives. Service businesses build cost increases into contract renewals, subscription pricing, and periodic repricing cycles. The April services PPI surge will be showing up in consumer-facing services prices through May, June, and into the summer.

Tariff pass-through acceleration: Trade services PPI rising 2.7% in a single month suggests that tariff costs — which were expected to affect consumer prices gradually — are flowing through supply chains faster than some models projected. The April 2 pharmaceutical tariff announcement, the ongoing goods tariffs on most trading partners, and the secondary effects on logistics and distribution are all visible in the April PPI. These costs will continue to flow downstream in May.

The combination of these three channels suggests that the 3.8% CPI of April is more likely the beginning of a re-acceleration than a peak.

The next CPI report covers May prices and releases on June 10. Given the PPI data from this week, the probability that May CPI comes in above April’s 3.8% is meaningfully higher than the probability it comes in below it.

What Smart Money Is Doing With This Data

The institutional response to Tuesday’s CPI and Wednesday’s PPI has been consistent across the major macro funds and fixed income desks.

Selling duration. Long-duration Treasury bonds — 10-year, 20-year, 30-year — are most sensitive to inflation expectations. When inflation expectations rise, bond prices fall and yields rise. With PPI at 6% and rate hike odds at 39%, the trade is to reduce exposure to the bonds most vulnerable to yield increases and the asset price losses those increases produce.

Buying short-duration inflation protection. Short-term Treasury Inflation-Protected Securities — TIPS with 1-3 year maturities — provide direct inflation compensation without the duration risk of longer-term bonds. In an environment where inflation is re-accelerating and the Fed may hike, short-duration TIPS are the rare asset class that benefits from both the inflation and the rate increase simultaneously.

Maintaining energy exposure. The PPI data confirms what the CPI data showed: energy is the driver, and the Strait of Hormuz remains effectively closed. Oil back near $100, the Iran peace offer rejected Sunday, only 13 Strait crossings on Sunday. The macro condition that is generating PPI and CPI upside surprises has not changed. Energy sector equities that performed +37.91% in Q1 have the same fundamental tailwind in Q2.

Increasing cash and short-term instruments. With rate hike probability at 39% and the Fed’s next decision not until June 17 — Kevin Warsh’s first meeting — the uncertainty about the direction of rates argues for preserving optionality. Money market funds paying 4.8-5% annualized are providing real returns above core CPI in a world where core CPI is 2.8%. In a world where the next rate move might be a hike rather than a cut, locking into duration is a risk that the PPI data has made considerably more expensive to take on.

The Real Cost Running Through Every Receipt

Here is the personal finance translation of Tuesday’s and Wednesday’s numbers.

The American household spending $800 per month on groceries in January 2026 is spending approximately $825-835 per month in April — a monthly increase of $25-35, or $300-420 annually from food inflation alone.

The American commuting 15,000 miles per year in a vehicle getting 28 miles per gallon is spending approximately $800 more per year on gasoline than they were before the Iran war — based on the $1.50+ per gallon increase from pre-war prices.

The American with a summer flight booked is paying 20.7% more in airline fares than a year ago — on average $80-150 more per round trip depending on the route.

The American with a $500 monthly credit card balance is paying approximately $110 per month in interest at current 22% average rates — and if the Fed hikes, that 22% becomes 22.5% or 23%, adding $5-10 more per month.

Individually, none of these numbers is catastrophic. Together, for the American earning the median wage of approximately $56,000 annually (after tax: approximately $45,000), they represent $1,500-2,000 in additional annual costs — roughly 3.3% to 4.4% of after-tax income — from inflation alone, before any of the structural cost increases in rent, insurance, and healthcare that have been building for years.

Real average hourly wages slipped 0.5% for the month and fell 0.3% annually. The paycheck is not keeping pace with the price increases.

That is what the “double squeeze” means in household budget terms. That is what 3.8% CPI and 6.0% PPI means at the kitchen table.

The Week That Defined the Second Half of 2026

By Friday afternoon, between the CPI, the PPI, and the retail sales and import price data still to come Thursday, the macro picture for the second half of 2026 will be considerably clearer than it was a week ago.

What is already clear from Tuesday and Wednesday: inflation is not decelerating. It is re-accelerating at both the consumer and producer level. The war in Iran is a significant driver but not the only one — services inflation, tariff pass-through, and shelter costs are all contributing to a broadening of price pressures that goes beyond the energy shock.

The Fed’s impossible position — described in the Powell last-press-conference post — has not improved with this week’s data. It has deteriorated. The 39% rate hike probability is the market’s assessment of how much worse the impossible position has become since Wednesday morning.

Kevin Warsh takes the chair on Thursday, May 15. His first policy decision comes at the June 17 FOMC meeting — just under five weeks from now. He will have one more CPI report before that decision, covering May prices. If May CPI comes in above April’s 3.8%, given the PPI signals, his first meeting will be the most consequential debut for a new Fed Chair since Paul Volcker walked into the job in August 1979.

Volcker raised rates. Dramatically. Into a recession. And broke the inflation of the 1970s.

Whether Warsh is willing to do the same, with consumer confidence at a 75-year low and the household survey showing employment losses — is the question that 39 cents on every dollar in rate hike probability is currently asking.

This is not financial advice. Always consult a qualified financial advisor before making significant financial decisions. If this week’s inflation data surprised you — or confirmed what you’ve been feeling at the grocery store and the gas pump — share this with someone who only saw the CPI headline. The PPI is the number that tells you where prices are going next. And subscribe below for the next one.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

Every single day — including today, including yesterday, including every day since October — the United States Treasury has been writing a check for $3 billion.

Not $3 billion for defense. Not $3 billion for Social Security. Not $3 billion for roads, hospitals, schools, or the military.

$3 billion per day, every day, just in interest on money already borrowed. Money that produces nothing new. Money that buys no goods, funds no programs, and employs no one. Just the cost of carrying the debt that already exists.

The Congressional Budget Office released its monthly budget update on May 8. The headline number: the US Treasury has paid $628 billion in net interest in the first seven months of fiscal year 2026 — the seven months between October and April. That works out to $89.7 billion per month, $20.7 billion per week, $2.97 billion per day.

$3 billion a day.

For context: $628 billion in seven months for interest payments is more than the US has spent on Medicare in the same period. Medicare — the program that provides healthcare to 67 million elderly and disabled Americans — cost $588 billion in those seven months. The debt’s interest bill exceeded it by $40 billion.

The numbers are almost impossible to process at human scale. So let’s try a different frame. In the time it takes to read this sentence, the US Treasury paid approximately $104,000 in interest. By the time you finish this post, it will have paid more than $3 million.

Tomorrow morning at 8:30 AM, the Bureau of Labor Statistics releases the Consumer Price Index for April 2026. That number — one statistic, released in one moment — will determine whether the $3 billion daily interest burden gets worse over the coming months, or whether it has any path toward relief.

Here is why the connection matters, why almost nobody is explaining it clearly, and what Tuesday’s number actually means for the fiscal situation that is quietly consuming the American government’s capacity to function.

How Inflation and Debt Interest Are the Same Problem

Most people understand inflation and government debt as separate issues. Politicians discuss them separately. Economic reporters cover them separately. The Fed talks about inflation; Congress talks about the deficit; rarely do the two conversations converge into a single, coherent picture.

But they are not separate. They are the same problem, expressed in two different ways. And understanding how they connect is the most important thing you can know about the economic environment of 2026.

Here is the mechanism.

The United States carries approximately $29 trillion in debt held by the public — the portion of the $39 trillion total that is owned by investors, pension funds, foreign governments, and other market participants outside the government itself. That debt carries interest rates that range from near-zero (on bonds issued during the COVID era when rates were suppressed) to approximately 4.5-5% (on bonds issued in the current high-rate environment).

As the low-rate bonds mature — as the debt issued in 2020, 2021, and 2022 at 0.5-1.5% interest comes due — the Treasury must refinance it at current rates. A $1 trillion bond maturing at 1% interest that is refinanced at 4.5% interest generates approximately $35 billion in additional annual interest expense with no additional borrowing. The debt doesn’t grow; it just gets more expensive.

This is called “interest rate rollover risk.” And it is the primary mechanism by which the $628 billion in seven-month interest payments will continue to grow even if the government stops adding new debt tomorrow.

The CBO’s projections show interest costs rising from $628 billion in seven months to somewhere between $900 billion and $1 trillion for the full fiscal year 2026. By fiscal year 2035, the CBO projects interest payments exceeding $2 trillion annually — roughly double today’s pace.

Now here is where Tuesday’s CPI connects.

Inflation drives interest rates. When inflation is high, bond investors demand higher yields to compensate for the erosion of purchasing power. When inflation falls, yields can fall, and the rollover problem becomes less severe. When inflation rises, yields rise with it, and every Treasury bond that matures and gets refinanced locks in higher costs for the next 2, 5, 10, or 30 years.

The CPI print on Tuesday is not just about gas prices and grocery bills. It is about the trajectory of the interest rate at which the US government is rolling over $8-10 trillion in debt annually. Every 25 basis points of additional yield on that rollover represents approximately $20-25 billion in additional annual interest expense.

Tuesday’s number, in other words, will tell us how much more expensive the $3 billion daily interest burden is about to become.

What the Market Expects Tuesday — And Why It Matters

The consensus forecast for April CPI, based on Wall Street economist surveys, is approximately 3.2-3.4% year-over-year, with a monthly increase of approximately 0.3%.

If that forecast is accurate, it represents a modest improvement from March’s 3.3% annual rate and 0.9% monthly surge. The March number was heavily distorted by the initial oil price shock from the Iran war — gasoline prices jumped 21.2% in March alone. April’s gasoline prices stabilized somewhat as the ceasefire (however fragile) allowed some temporary relief. A lower monthly CPI in April would partly reflect that stabilization.

But the consensus forecast also comes with an unusual degree of uncertainty. The Iran war’s economic impact continues to ripple through supply chains, food prices, and energy costs in ways that are difficult to model precisely. The pharmaceutical tariffs announced on April 2 began to flow through drug prices in April. Shipping costs from Strait of Hormuz disruption affect goods prices with a lag of 60-90 days — meaning March’s disruption shows up in April-May retail prices.

The range of economist forecasts for Tuesday’s print spans from 2.8% to 3.7% annual — a genuinely wide range that reflects genuine uncertainty about which forces are dominating in the April data.

Here is what each scenario means.

If April CPI comes in below 3.0%:

A significant downside surprise would be the most positive development the Fed and the Treasury have seen in months. It would signal that March’s 0.9% monthly surge was indeed a temporary oil shock rather than the beginning of re-acceleration. Bond yields would likely fall, reducing the rollover cost for new Treasury issuance. The probability of a Fed rate hike — currently priced at roughly 25% by futures markets — would fall significantly. The daily interest burden would still be $3 billion, but the trajectory would shift toward relief rather than escalation.

If April CPI comes in between 3.0% and 3.5% (consensus):

An in-line result would produce limited market reaction. The Fed would remain on hold. Bond yields would remain elevated. The rollover cost would remain high. The $3 billion daily interest burden would continue on its current trajectory toward $1 trillion annually. The status quo — uncomfortable but not acute — would persist.

If April CPI comes in above 3.5%:

An upside surprise — driven by food price pass-through from the Strait disruption, pharmaceutical tariff impacts on healthcare costs, or service sector inflation that has proved persistent — would be the most damaging scenario for the debt trajectory. Bond yields would likely rise, increasing the rollover cost. The probability of a Fed rate hike would increase. The $3 billion daily interest figure would begin moving toward $3.5 billion, then $4 billion, as each new bond issuance gets refinanced at higher rates. The CBO’s projection of $2 trillion in annual interest by 2035 would look optimistic rather than alarming.

The Number Bigger Than Medicare That Nobody Is Discussing

The fiscal picture that the CBO’s May 8 update reveals deserves to be stated simply, because the individual numbers are so large that the overall picture gets lost.

The US government’s largest expenditure categories in the first seven months of fiscal year 2026:

Social Security: $953 billion

Medicare: $588 billion

Net interest on public debt: $628 billion

Medicaid: $409 billion

Defense: approximately $600 billion

Net interest on the public debt — $628 billion for seven months — now exceeds Medicare. It exceeds Medicaid by more than 50%. It is approaching defense spending.

This is a category of government expenditure that produces nothing for the American public. It does not feed anyone, heal anyone, defend anyone, or educate anyone. It is the price of past decisions — borrowing to fund tax cuts, stimulus programs, wars, and ongoing deficit spending — extracted in the present.

The deficit so far this year is actually smaller than it was for the same period a year prior — one of the few pieces of relatively positive fiscal news in the CBO update. But that improvement is occurring on top of a base interest burden that is already historically unprecedented in peacetime and that will grow regardless of current deficit trends as long as interest rates remain elevated.

Outlays for net interest on the public debt rose by $41 billion, or 7 percent, because the debt was larger than it was in the first seven months of fiscal year 2025.

A 7% year-over-year increase in interest payments. In a year when the government has a smaller deficit than the prior year. The interest burden is growing faster than efforts to control it, because the debt stock is large enough that even modest growth in the principal base generates significant interest cost increases at current rates.

The Structural Problem That Tuesday’s CPI Won’t Fix

Tuesday’s CPI print matters. But even a perfect, below-consensus reading won’t change the structural fiscal situation that the $3 billion daily number represents.

The structural problem is the relationship between the interest rate, the debt stock, and economic growth.

For a government’s debt to be sustainable — for the ratio of debt to GDP to remain stable or improve — the economy needs to grow faster than the real interest rate on its debt. When growth exceeds interest rates, the debt becomes smaller relative to the economy even without paying it down directly. This is the mechanism by which the United States reduced its debt-to-GDP ratio significantly after World War II — rapid economic growth outpaced interest costs.

Right now, the relationship is inverted. The real interest rate on US government debt (nominal yield minus inflation) is approximately 1-1.5%. The real GDP growth rate is approximately 0-1% after stripping out the one-time factors from Q1’s 2.0% nominal print. An economy growing at 0-1% in real terms, carrying debt at 1-1.5% real rates, is in a situation where the debt ratio grows even with no new borrowing.

The CBO director told Fortune earlier this year that “productivity is massively the most important thing” for the long-term fiscal outlook. If AI generates the productivity gains that the $650 billion annual capex commitment is predicated on — if the economy grows at 3-4% real rates as AI-driven productivity compounds — the fiscal picture changes dramatically. The debt becomes manageable. The $3 billion daily interest payment becomes a smaller share of a much larger economic base.

If AI doesn’t deliver those gains — if the productivity revolution takes longer than the investment cycle assumes, or doesn’t materialize at the scale projected — the fiscal picture becomes increasingly difficult. The interest payments grow. The debt ratio grows. The government’s capacity to respond to the next crisis — war, pandemic, recession — becomes increasingly constrained.

Tuesday’s CPI is one data point in that larger story. It is the most important single data point of the week. But it is one data point.

Iran, the Strait, and the Interest Bill

There is a direct line from the Strait of Hormuz to the US Treasury’s interest payment.

It runs like this.

The Strait of Hormuz remains effectively closed. Oil is back near $100 after the peace offer was rejected Sunday — Iran held the same demands it had made previously, including reparations and control over the Strait. Trump rejected it. Only 13 Strait crossings occurred on Sunday, 3 on Saturday. Flows remain at a trickle.

As long as oil is near $100, inflation stays elevated. As long as inflation stays elevated, the Fed cannot cut rates. As long as the Fed cannot cut rates, Treasury bond yields remain near 4.3-4.5%. As long as yields remain near 4.3-4.5%, every bond that matures and is refinanced locks in higher interest costs than the bond it replaces. As long as each bond locks in higher costs, the annual interest burden grows.

The $628 billion in seven months becomes $950 billion for the full year. Then $1.1 trillion. Then, as the CBO projects, $2 trillion by 2035.

The Strait of Hormuz and the US Treasury’s interest bill are connected by the same chain. It takes about four steps to trace the connection. But it is a direct causal chain, not a correlation.

Tuesday’s CPI is one measurement of where that chain currently stands. Is oil’s inflation already flowing fully through into core prices? Or is the pass-through still incomplete, with more to come in May and June?

The answer to that question — expressed as a single percentage at 8:30 AM Tuesday — will shape the trajectory of the $3 billion daily interest burden for the next six months.

What To Watch This Week Beyond CPI

Tuesday’s CPI is the main event. But the week’s data calendar is unusually rich for anyone tracking the intersection of inflation and fiscal pressure.

Wednesday: PPI (Producer Price Index). The Producer Price Index measures inflation at the wholesale level — the prices that businesses pay before they pass costs to consumers. PPI tends to lead CPI by 30-60 days. A high PPI on Wednesday signals that whatever Tuesday’s CPI shows, more inflation is in the pipeline. A low PPI suggests the pass-through is moderating.

Thursday: Import prices, jobless claims, retail sales. Import prices measure inflation arriving from overseas — including from the supply chains disrupted by the Strait closure and affected by tariff pass-through. Retail sales show whether the American consumer is still spending despite the inflation squeeze. Jobless claims will update the labor market picture from the confusing April report. All three in one day.

Friday: Industrial production. The health of the manufacturing sector, which has been in the ISM’s expansion territory for four consecutive months but faces headwinds from trade uncertainty and input cost inflation.

The week’s data, taken together, will be the most comprehensive single-week read on the American economy since the quarter began. By Friday afternoon, the picture of whether the Iran war’s economic damage is stabilizing or accelerating will be considerably clearer than it is today.

The Bottom Line for May 11, 2026

The United States Treasury paid $628 billion in interest in the first seven months of fiscal year 2026 — $3 billion per day, more than it spent on Medicare. Powell’s term as Fed Chair ends Thursday, May 15. Kevin Warsh takes over with an inflation mandate that the $3 billion daily figure makes impossible to compromise on. Iran rejected the peace offer Sunday and Trump rejected their counter. Oil is back near $100. The Strait is at a trickle.

Tomorrow morning at 8:30 AM, one number will tell us whether this situation is stabilizing or accelerating.

The number that matters is not the headline. It is whether core CPI — the measure that strips out food and energy and reveals the underlying inflation that monetary policy is supposed to address — is above or below the prior month’s reading.

If core CPI is decelerating: the bond market exhales, yields fall modestly, the rollover cost pressure moderates, Warsh inherits a slightly more manageable situation.

If core CPI is accelerating: yields rise, rate hike probability increases, the rollover cost accelerates, and the $3 billion daily number begins moving toward $3.5 billion.

$3 billion per day. Every day. Just in interest.

Tomorrow morning, we find out if that’s the floor or the ceiling.

This is not financial advice. Always consult a qualified financial advisor before making significant financial decisions. If this helped you understand why tomorrow’s inflation number matters beyond your grocery bill — share it before 8:30 AM Tuesday. The number that shapes the US government’s finances for the next decade drops in less than 24 hours. And subscribe below for the next one.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

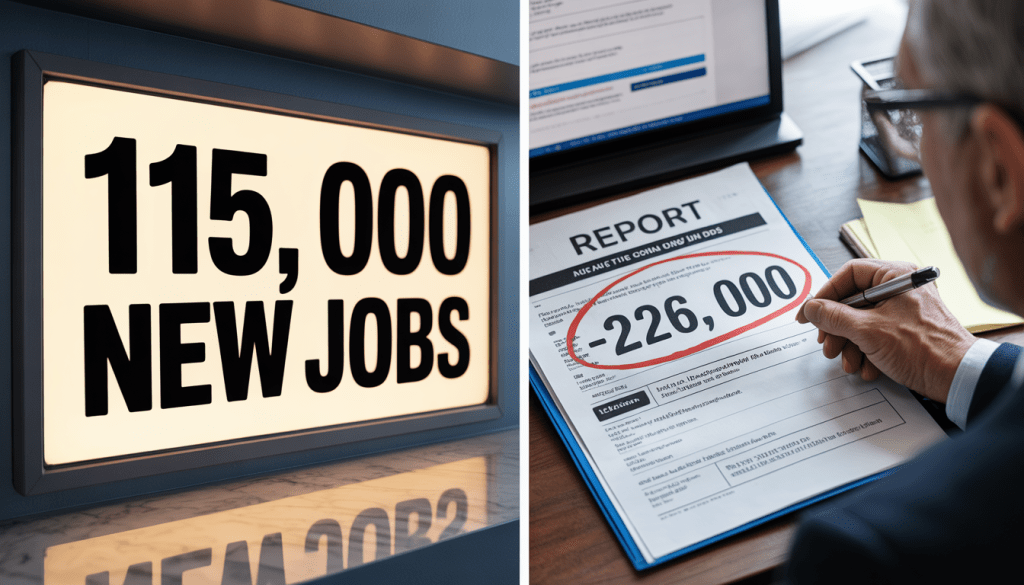

This morning, the Bureau of Labor Statistics released the April jobs report.

The headline number was 115,000 new jobs. Better than the 55,000 consensus. Unemployment unchanged at 4.3%. Markets breathed. Anchors said “resilient.” The word “solid” appeared hundreds of times in financial news coverage within the hour.

And buried in the same report — released at the exact same moment, from the exact same agency — was a different number.

Negative 226,000.

Not 115,000 new jobs. Minus 226,000 workers. A loss. In April.

Both numbers are real. Both are official. Both come from the Bureau of Labor Statistics. They measure slightly different things, using slightly different methodologies, and they have never diverged this sharply for this many consecutive months without it eventually meaning something important.

The 115,000 is the number that will trend. The -226,000 is the number that will explain why, six months from now, the economy looks worse than today’s headlines suggested.

Here is what is actually happening inside the April jobs report that nobody is explaining clearly.

Two Surveys. Two Completely Different Stories.

The monthly jobs report contains data from two separate surveys conducted by the BLS. Most people don’t know this. Most financial coverage doesn’t explain it clearly enough. And the divergence between them, in April 2026, is the most important story in today’s data.

The Establishment Survey — the one that produced +115,000 — surveys approximately 119,000 businesses and government agencies. It asks employers how many people are on their payroll. It is the source of the headline number. It is the most widely reported figure. It tends to be more stable month-to-month but is subject to significant revisions (as documented in the previous post’s -911,000 benchmark revision discussion).

The Household Survey — the one that produced -226,000 — is a separate survey of approximately 60,000 households. It asks people directly whether they are employed, unemployed, or not in the labor force. It is the source of the unemployment rate. It tends to be noisier month-to-month but captures important dimensions of labor market reality that the establishment survey misses: the self-employed, agricultural workers, private household workers, and — critically — people who work multiple jobs (counted once in the household survey, multiple times in the establishment survey).

In a functioning, stable labor market, the two surveys tell roughly the same story over time. Month-to-month divergences are normal. But sustained divergence — the household survey consistently painting a darker picture than the establishment survey — is a warning signal that experienced labor market analysts take seriously.

The household survey has now shown a loss of employment in every single month of 2026. January, February, March, April — four consecutive months of household survey employment declines. The establishment survey has shown gains in every month except February.

Four consecutive months of divergence in the same direction is not statistical noise. It is a pattern. And the pattern says: the people being surveyed are telling the BLS they don’t have jobs at the same time that the businesses being surveyed are telling the BLS they have workers on payroll.

The 3-Month Average That Changes Everything

When the April headline of +115,000 is announced, it will be compared to the prior month’s +185,000 (March, after upward revision). The month-over-month comparison looks fine. Slower, but positive.

But the three-month rolling average — which smooths out the extraordinary month-to-month volatility that has characterized 2026 labor data — tells a completely different story.

Revisions pulled down the three-month average for job gains to 48,000 per month.

48,000 per month. That is the actual pace of job creation in the United States, averaged across the past three months including today’s revisions.

For context: economists estimate that approximately 100,000-120,000 new jobs per month are needed to absorb new labor force entrants and keep the unemployment rate stable — given current labor force growth constraints from demographics and immigration policy. A three-month average of 48,000 is less than half the breakeven rate.

An economy creating jobs at less than half the rate needed to keep pace with labor force growth should, in theory, be producing a rising unemployment rate. The unemployment rate is not rising — it is holding at 4.3%.

Why? Because the labor force is shrinking. People are leaving. They are not being counted as unemployed because they have stopped looking for work. And when people stop looking for work, they fall out of the unemployment calculation entirely.

This is the most important number in today’s report that is receiving almost no attention.

The labor force participation rate has declined from 62.6 to 61.8 percent. The labor force — the total number of people either employed or actively looking for work — has declined by more than 1 million. And the number of people employed has declined by more than 1.2 million.

The labor force shrank by over a million people. The number of employed people fell by over 1.2 million. These are the household survey numbers. They describe an America where people are not losing their jobs in mass layoffs — they are quietly leaving the workforce entirely.

The Real Unemployment Rate: 8.2%

The headline unemployment rate is 4.3%. That number gets the attention, the graphic, the anchor’s commentary.

But the BLS produces a second, broader unemployment measure every month — the U-6. It is not hidden. It is published in the same report. It includes, in addition to the officially unemployed, two additional groups that the headline rate excludes: marginally attached workers (people who want jobs and have looked in the past year but not in the past four weeks) and people working part-time for economic reasons (people who want full-time jobs but can only find part-time work).

The U-6 measure, now at 8.2%, captures some of this shift in individuals leaving the labor force.

8.2% is the real unemployment rate. The one that counts the people who have given up looking. The one that counts the people who took a part-time job because they couldn’t find a full-time one.

That is two full percentage points above what we saw in 2019.

In 2019, the labor market was considered historically strong. Economists were using phrases like “the best job market in 50 years.” U-6 was around 6.2%.

Today, with the headline unemployment rate matching 2019 levels (4.3%), the U-6 is two full percentage points higher. That gap — between the headline rate and the broader reality — represents millions of Americans who are counted as “not unemployed” but are clearly not experiencing the labor market conditions that the headline number implies.

Those who were forced to accept part- instead of full-time work rose by 445,000 in April alone.

445,000 Americans moved from full-time employment to involuntary part-time in a single month. These are workers who did not lose their jobs in the technical sense — they are still employed, still counted in the headline 115,000 — but whose income, hours, and economic security deteriorated significantly.

The AI Job Destruction Nobody Is Naming Directly

Buried in the sector breakdown of today’s report is a data point that should be generating considerably more discussion than it is.

Information services lost 13,000 jobs in April, part of a continuing trend that has seen the category down 342,000 jobs since November 2022, coinciding with the rise of artificial intelligence.

342,000 jobs lost in information services since November 2022. The timing is not ambiguous — November 2022 is when ChatGPT launched and the generative AI era began in earnest. The information services sector, which includes software publishing, data processing, and other technology-adjacent roles that are most directly exposed to AI substitution, has lost 342,000 jobs in the same period that the largest technology companies in the world have been deploying AI across their operations.

These are not manufacturing jobs, not retail jobs, not hospitality jobs. These are white-collar, knowledge-economy jobs — the category that was supposed to be safe from automation, that was supposed to benefit from AI as an assistive tool rather than being replaced by it.

342,000 jobs in one sector. Over 30 months. At an accelerating pace.

The White Collar Bloodbath post in this series, published in March, documented the wave of AI-driven layoffs at McKinsey, Salesforce, Microsoft, Nvidia, and other major employers. Today’s BLS data is the first official government confirmation that the pattern is real and is showing up in aggregate employment statistics.

Information services employment down 342,000 since AI launch. Not a forecast. An official government measurement.

Who Is Actually Leaving the Labor Force

The labor force participation rate fell to 61.8% in April — the lowest since October 2021. More than 1 million people left the labor force in a year. The question of who is leaving is as important as the fact that they are leaving.

Men over the age of 55 and prime age women — those 25 to 54 — accounted for the losses.

Two distinct groups. Two entirely different reasons.

Men over 55: Early retirement, voluntary and involuntary. In a labor market where knowledge-economy jobs are being eliminated by AI and knowledge-economy workers over 55 face significant age discrimination in re-employment, the choice between continued job searching and early retirement is not always voluntary. Many of the men leaving the labor force are not choosing leisure — they are accepting that re-employment at comparable compensation is unlikely and taking the Social Security and pension income available to them.

Prime age women (25-54): The childcare and return-to-office collision.

Prime age women with a bachelor’s degree or higher and small children at home have been dropping out of the labor force entirely in response to the high costs of childcare and return-to-office mandates.

This is one of the most consequential economic trends in the current data — and it is almost entirely invisible in the headline number.

Childcare costs have risen to the point where the math of working full-time while paying for childcare is, for many families, negative. A family with two young children in a major metropolitan area can face childcare costs of $3,000-4,000 per month. For a parent earning $60,000-75,000 annually, the post-tax income net of childcare is close to zero — or actually negative after commuting and other work-related costs.

Simultaneously, the return-to-office mandates that major employers have implemented in 2025-2026 have eliminated the flexibility that made dual-income households with young children mathematically viable. Remote work allowed a parent to be geographically available during school pickup windows, sick days, and school closures without burning vacation time. The elimination of remote flexibility, in a world of $3,000-4,000 monthly childcare costs, is pushing prime-age women out of the workforce in a pattern that the April data makes visible.

The eldercare market is in crisis. Men make up almost half of all unpaid elder care providers.

The men over 55 who are leaving the labor force are not only retiring. Many are becoming unpaid caregivers for aging parents in a healthcare system where professional elder care is increasingly unaffordable. This is the hidden demographic crisis inside the labor force participation rate.

Federal Employment: Down 348,000 From Peak

Federal employment is now down 348,000 jobs from its peak in October 2024. Staffing shortages have become acute at some federal agencies; older workers took buyouts, early retirement and quit in the wake of last year’s cuts.

348,000 federal jobs eliminated since October 2024. This is the DOGE effect made numerical and official.

The cuts are not evenly distributed. They are concentrated in regulatory agencies, research institutions, social service administration, and the federal workforce that implements programs — not the military or law enforcement functions that have been protected or expanded.

The consequences of this concentration are beginning to show up in ways that the employment statistic doesn’t capture. Staffing shortages at the Social Security Administration affect processing times for disability and retirement claims. Shortages at the Veterans Administration affect service delivery to veterans. Shortages at the FDA affect drug approval timelines — the same FDA that is simultaneously being asked to certify new US pharmaceutical manufacturing facilities in the context of the pharmaceutical tariff transition.

The 348,000 federal job losses are in the headline establishment survey. They are one reason the overall headline looks worse than it might otherwise — federal employment has been a persistent drag on an otherwise positive private sector picture.

But the economic impact of those 348,000 jobs extends well beyond the employment statistic. The services those workers provided don’t stop being needed just because the workers are gone.

The Housing Market Signal Hidden in Plain Sight

The residential building construction sector lost 1,500 jobs and residential specialty trade contractors shed 8,900 positions. Real estate also lost jobs in April, with employment falling by 1,700 jobs, while rental and leasing services employment fell by 3,600 jobs.

These are small numbers relative to the 115,000 headline. But they are directionally significant.

Residential construction employment falling — in a month that should be seeing seasonal strength as spring building season begins — signals that homebuilders are pulling back on activity. With mortgage rates at 6.75-7%, the economic math of homebuilding has deteriorated. Builders who started projects at lower rates are completing them. New project starts are declining.

Real estate employment falling — agents, brokers, property managers — reflects the transaction volume collapse that accompanies high mortgage rates. Fewer transactions mean less commission income, which means fewer employed real estate professionals. The housing market contraction that the MBA has been documenting for months is now showing up in employment data.

The Fed’s “higher for longer” policy, maintained to fight the inflation that the Iran war has re-accelerated, is producing a housing market contraction that is measurable in construction and real estate employment. The homebuyer who is waiting for rates to fall is waiting for a Fed that cannot cut. And the workers who depend on housing market activity are feeling the consequences.

What The Numbers Together Actually Say

The April 2026 jobs report, read in full, says this:

The establishment survey shows 115,000 new hires — employers adding workers to payrolls at a rate better than consensus, concentrated in healthcare, transportation, and retail.

The household survey shows 226,000 fewer employed people — workers reporting to surveyors that they don’t have jobs, even as employers report them on payrolls.

The labor force shrank by over a million people over the past year. The people leaving are not being counted as unemployed. The unemployment rate holds at 4.3% not because the labor market is strong but because the denominator — the number of people looking for work — is falling.

The U-6 “real” unemployment rate is 8.2%. Two percentage points above 2019. 445,000 Americans moved from full-time to involuntary part-time in April alone.

Information services has lost 342,000 jobs since AI launched in November 2022. Federal employment is down 348,000 from its October 2024 peak. Residential construction and real estate shed jobs in what should be the spring building season.

The three-month average payroll gain — after today’s revisions — is 48,000. Less than half the breakeven rate.

This is the jobs report that the headline number is not describing. Both are true. The 115,000 is real. The rest of this is also real.

The question is which truth more accurately describes the economic experience of the 160 million Americans in the labor force.

The consumer confidence data — at a 75-year low — suggests they have already voted on that question.

This is not financial advice. Always consult a qualified financial advisor before making significant financial decisions. If this gave you a clearer picture of what was actually inside this morning’s jobs report beyond the headline — share it with someone who heard “115,000” and thought the economy was fine. And subscribe below for the next one.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

This morning at 8:30 AM Eastern, the Bureau of Labor Statistics will release the April 2026 jobs report.

Markets will react. Anchors will comment. The headline number will trend. Everyone will form an opinion about whether the economy is strong or weak based on a single number released at a single moment.

But before you read that number — before you decide what it means — there is something you need to understand about the numbers that came before it.

Last month, buried in the technical footnotes of the March employment release, the Bureau of Labor Statistics published a sentence that deserved front-page coverage and received almost none.

The preliminary benchmark revision for March payroll employment is -911,000 (-0.6%).

Nine hundred and eleven thousand jobs. Gone. Not lost — never there. They were in the official monthly reports. They were cited by economists and politicians and financial media as evidence of labor market strength. They were the basis for Federal Reserve decisions about interest rates. They were the numbers that shaped the narrative about the American economy throughout 2025.

And they were wrong. The government overcounted employment by 911,000 people.

Today’s April report will generate enormous coverage. This context will generate almost none. That gap is the most important thing to understand about the jobs data you’re about to read.

What a Benchmark Revision Actually Is — And Why This One Matters

Every spring, the Bureau of Labor Statistics conducts what it calls a “benchmark revision” — a comprehensive reconciliation of its monthly employment estimates against complete payroll tax records from state unemployment insurance systems. This is the definitive count. It covers every employer, every payroll, every W-2 filed in the United States.

The monthly jobs reports — the ones that move markets and dominate headlines — are estimates. They are based on surveys of approximately 119,000 businesses representing about 26% of nonfarm payroll jobs. The estimates are constructed using statistical models and seasonal adjustment factors. They are the best available real-time approximation of what is happening in the labor market.

The benchmark revision is the correction that happens when the approximation meets the reality.

The -911,000 preliminary revision means that between April 2024 and March 2025, the BLS overestimated employment by 911,000 workers. On a base of approximately 158 million nonfarm payroll jobs, that is a 0.6% overcount — within the BLS’s stated margin of error, technically acceptable, but economically significant.

Here is why it matters beyond the statistical footnote.

The Federal Reserve made interest rate decisions based on this data.

Throughout 2025, as the Fed was navigating whether to cut rates and by how much, the official employment numbers showed a labor market that was stronger than it actually was. The FOMC members who voted on rate decisions were looking at employment figures that were overstated by nearly a million workers.

A million workers is not a rounding error. It is the difference between a labor market that is genuinely resilient and one that was softer than the reported numbers suggested. It is the difference between an economy that can absorb higher rates without significant damage and one that was already under more stress than the data indicated.

The Fed cut rates three times in late 2025. Would those decisions have been different — perhaps more aggressive, cutting sooner or by more — if the employment data had been accurate in real time? Nobody can say with certainty. But the question matters because the policy decisions compound. Rate decisions made in late 2025 based on data that was subsequently revised by 911,000 workers shaped the economic conditions that the Iran war then hit in early 2026.

This Is Not the First Time. It’s Getting Worse.

The -911,000 revision is large. But it is not unprecedented. It follows a pattern that has been building for several years.

In 2024, the BLS’s preliminary benchmark revision showed that the prior year’s employment had been overstated by 818,000 workers — the largest downward revision since 2009.

In 2023, the revision was smaller — approximately 300,000 — but still directionally negative.

In 2022, another negative revision of several hundred thousand.

The pattern is consistent: for four consecutive years, the monthly employment estimates have overstated actual employment, and the annual benchmark revision has corrected the overcount downward. Every year, the narrative of labor market strength that was built on the monthly estimates has been quietly revised to reflect a reality that was somewhat weaker than advertised.

Why is this happening systematically? The explanations that labor statisticians offer are technical: changes in birth/death model adjustments, difficulty capturing employment in new business formations, challenges measuring gig economy and contract work that doesn’t show up cleanly in traditional payroll survey frameworks.

But the systematic directionality — always overstating, never understating, for four consecutive years — is harder to explain purely on technical grounds. A random measurement error would produce revisions in both directions roughly equally. Four consecutive years of overstatement suggests a structural bias in the methodology that is consistently producing numbers that are too strong.

That structural bias has consequences. It creates an economy that looks stronger in real time than it is. It creates a Fed that may be acting on a more optimistic employment picture than the eventual data supports. And it creates a public narrative about economic health that is consistently revised downward months after the fact, when the corrections receive a fraction of the attention given to the original releases.

February Was Revised to -133,000. That Should Be a Bigger Story.

The benchmark revision covers a long period. But the most recent monthly revision — what the BLS does every month when it adjusts prior months as new data comes in — produced a number that deserves specific attention.

The February 2026 employment report was revised from the originally reported figure to -133,000 jobs. A loss of 133,000 jobs in a single month.

The original February report — the one that made headlines — showed a significant decline but was understood as partly war-related, partly seasonal. The revised figure of -133,000 is considerably worse than the original reading.

For context: in the entire post-COVID expansion, monthly job losses of this magnitude have occurred only during specific acute shocks — the initial COVID collapse, the post-reopening volatility of 2021-2022. A -133,000 month in February 2026 is a genuine labor market contraction, not a rounding error.

January was revised upward by 34,000 — to +160,000 — which partially offsets the February deterioration. But the combined January-February picture is 7,000 jobs lower than previously reported. And the trend embedded in those revisions — a strong January followed by a sharp February contraction — describes a labor market that hit the Iran war in a more fragile state than the original numbers suggested.

The April Consensus: A Number That Reveals the Uncertainty

Today’s April jobs report arrives with an unusually wide range of forecasts from Wall Street economists — itself a signal about how uncertain the underlying picture is.

The consensus estimate is approximately 55,000 to 165,000 jobs, depending on which economist’s forecast you weight most heavily. That is an extraordinary spread. A 110,000-job range in a monthly forecast reflects genuine disagreement about the state of the labor market — disagreement that stems directly from the noisy, frequently revised data environment described above.

Wells Fargo economists estimate total payrolls advanced 70,000. Bank of America forecasts 80,000. Fifth Third Commercial Bank forecasts 120,000. The range across major institutional forecasters spans from 50,000 to 165,000.

The wide spread has a specific explanation. The March report — at +178,000 — significantly beat expectations, which themselves were clustered around 50,000-100,000. After a beat of that magnitude, forecasters are divided between those who expect a snapback lower and those who think March represents the start of a more durable acceleration.

Wednesday’s ADP private payrolls report — a different measure that covers only private sector employment — came in at 109,000, beating the 84,000 consensus estimate. Job creation was concentrated in education and health services, which added 61,000. Small companies with fewer than 50 employees added 65,000.

ADP’s chief economist described the result as “small and large employers are hiring, but we’re seeing softness in the middle” — a characterization that describes a labor market bifurcation that mirrors the broader economic K-shape this series has documented throughout the Iran war period.

A strong beat could reignite Fed rate hike bets. Traders currently price in a 25% chance of a rate hike in 2026.

That last sentence deserves to stand alone. A 25% probability of a rate hike — not a cut, a hike — in an economy where consumer confidence just hit a 75-year low. That is the Fed’s impossible position made numerical.

The Real Wages Story Nobody Is Leading With

Beyond the headline payroll number, there is a data series in the March employment report that received almost no coverage and that is more important for understanding the financial condition of American households than any jobs count.

Real average hourly earnings for all employees decreased 0.6 percent in March, seasonally adjusted.

Nominal wages increased 0.2 percent. CPI-U increased 0.9 percent. The difference — negative 0.7 percentage points — is the real wage destruction that happened in a single month.

Real average weekly earnings decreased 0.9 percent.

These are not annualized numbers. These are single-month declines in the purchasing power of the American worker’s paycheck. In March alone — driven by the 0.9% monthly CPI surge that the Iran war’s oil shock produced — the average American worker became measurably poorer despite receiving a nominal pay increase.

This is the mechanism behind the paradox documented in the previous post in this series: the 50-year-low in jobless claims coexisting with the 75-year-low in consumer confidence. People have jobs. Their paychecks are larger in nominal terms. Their purchasing power is falling in real terms. The job market statistic says strength. The real wages statistic says deterioration. Both are true simultaneously.

The April jobs report will show nominal wage growth. Watch the real wage figure — the number that adjusts for CPI. That number, not the headline payroll count, is the one that describes what is actually happening to the financial lives of working Americans.

What A Strong Number Means. What A Weak Number Means. What Both Mean.

The April jobs report will produce one of three broad outcomes and it is worth understanding what each one means before the number drops.

If April comes in above 150,000:

A beat would be interpreted as evidence of labor market resilience despite the Iran war. Markets would likely sell off on the news — because a strong jobs number makes Fed rate cuts less likely. Specifically, it would increase the probability of the “higher for longer” scenario that has been weighing on rate-sensitive sectors (technology, real estate, consumer discretionary) throughout the first quarter.

The irony of a strong jobs number pushing markets lower is the defining feature of the current economic environment. Normally, good economic data is good for markets. In a world where the Fed cannot cut rates and may need to hike them, good economic data removes the last remaining justification for rate relief.

The 25% market probability of a rate hike would likely increase on a strong beat.

If April comes in between 50,000 and 150,000:

An in-line result — consistent with the broad consensus range — would likely produce muted market reaction. It confirms the “low hire, low fire” labor market that has characterized the past two years without providing decisive evidence for either the optimistic or pessimistic scenario. The Fed’s impossible position remains unchanged. Rate uncertainty persists.

If April comes in below 50,000 — or negative:

A significant miss would reignite recession fears that have been building but not yet confirmed by official data. It would be the first piece of hard payroll data suggesting that the Iran war’s economic damage is moving beyond energy prices and consumer sentiment into actual job destruction.

A miss of this magnitude — combined with the -133,000 February revision, the 0.5% Q4 GDP, the potentially weak Q1 private sector growth, and the 75-year consumer sentiment low — would create the most compelling argument yet for emergency Fed action. But with core PCE at 4.3% and inflation expectations at 4.8%, “emergency action” in the form of rate cuts remains deeply problematic.

A weak April number in this specific inflation environment creates the possibility of the most difficult monetary policy decision in decades: whether to cut rates in a recession while inflation is running well above target.

The Three-Month Average That Tells the Real Story

Beyond today’s single-month April print, the number that matters most for understanding labor market trajectory is the three-month average of payroll growth.

Three-month average: approximately +68,000 per month.

68,000 per month is below the breakeven rate — the number of jobs needed to absorb new labor force entrants and keep the unemployment rate stable. Economists estimate that breakeven is approximately 100,000-120,000 per month given current labor force growth rates constrained by immigration policy changes and demographics.

If April comes in near the 55,000-80,000 range that the more cautious forecasters project, the three-month rolling average falls further below breakeven. The unemployment rate — currently at 4.3% — would begin drifting toward 4.5% and higher in subsequent months.

An unemployment rate moving consistently from 4.3% toward 4.5% and then 4.7% is not a catastrophe in isolation. But in the context of a war-driven inflation shock, a Fed that cannot cut rates, record consumer debt, and the worst consumer confidence in 75 years — it is the piece of the picture that converts all of the other warning signs from potential risk to confirmed deterioration.

What To Watch At 8:30 AM — And What The Number Won’t Tell You

When the number drops this morning, here is what to look for beyond the headline.

The headline payroll count. Yes, obvious — but note the range of estimates and where the actual print falls relative to the full range, not just the median consensus. A miss relative to the most optimistic forecast is a different signal than a miss relative to the median.

The revisions to March and February. March’s +178,000 was strong and may be revised lower, as previous months have been. February’s already-revised -133,000 may be revised further. The revision pattern over the past four years has been consistently downward — meaning today’s strong months often look weaker in subsequent reports.

Real average hourly earnings. Not the nominal number. The real number — nominal earnings growth minus CPI. This is the number that tells you whether the workers keeping their jobs are getting richer or poorer in purchasing power terms.

The government employment line. Federal employment has been declining as DOGE-related cuts flow through. Today’s number will show another month of federal employment contraction. Watch whether state and local government employment is offsetting federal declines, or whether the government sector as a whole is becoming a headwind to the headline number.

The unemployment rate. 4.3% is the current figure. Any movement above 4.3% — even to 4.4% — will receive outsized attention in a market that is already pricing a 25% probability of a rate hike and needs any evidence of economic softening to push that probability lower.