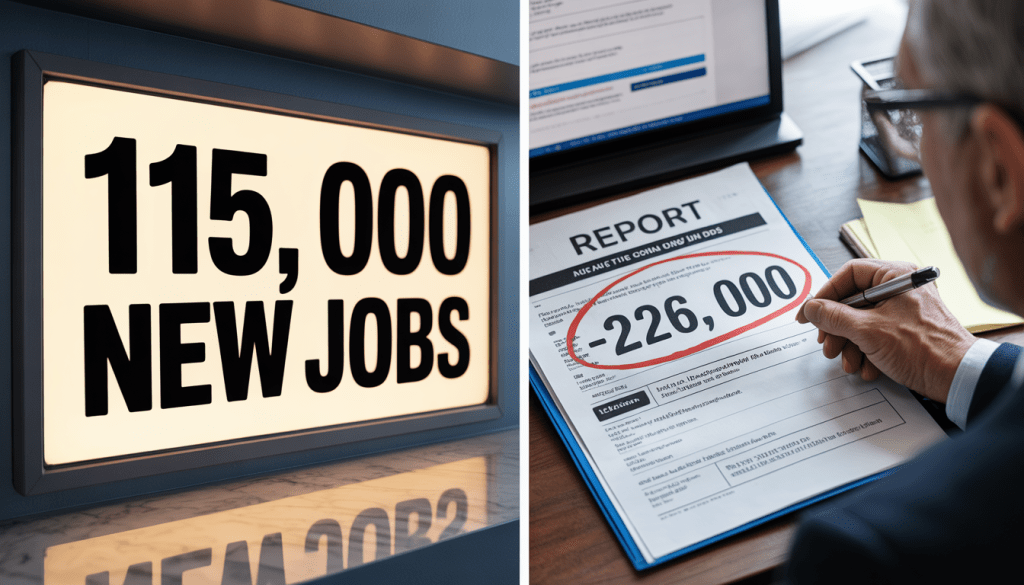

This morning, the Bureau of Labor Statistics released the April jobs report.

The headline number was 115,000 new jobs. Better than the 55,000 consensus. Unemployment unchanged at 4.3%. Markets breathed. Anchors said “resilient.” The word “solid” appeared hundreds of times in financial news coverage within the hour.

And buried in the same report — released at the exact same moment, from the exact same agency — was a different number.

Negative 226,000.

Not 115,000 new jobs. Minus 226,000 workers. A loss. In April.

Both numbers are real. Both are official. Both come from the Bureau of Labor Statistics. They measure slightly different things, using slightly different methodologies, and they have never diverged this sharply for this many consecutive months without it eventually meaning something important.

The 115,000 is the number that will trend. The -226,000 is the number that will explain why, six months from now, the economy looks worse than today’s headlines suggested.

Here is what is actually happening inside the April jobs report that nobody is explaining clearly.

Two Surveys. Two Completely Different Stories.

The monthly jobs report contains data from two separate surveys conducted by the BLS. Most people don’t know this. Most financial coverage doesn’t explain it clearly enough. And the divergence between them, in April 2026, is the most important story in today’s data.

The Establishment Survey — the one that produced +115,000 — surveys approximately 119,000 businesses and government agencies. It asks employers how many people are on their payroll. It is the source of the headline number. It is the most widely reported figure. It tends to be more stable month-to-month but is subject to significant revisions (as documented in the previous post’s -911,000 benchmark revision discussion).

The Household Survey — the one that produced -226,000 — is a separate survey of approximately 60,000 households. It asks people directly whether they are employed, unemployed, or not in the labor force. It is the source of the unemployment rate. It tends to be noisier month-to-month but captures important dimensions of labor market reality that the establishment survey misses: the self-employed, agricultural workers, private household workers, and — critically — people who work multiple jobs (counted once in the household survey, multiple times in the establishment survey).

In a functioning, stable labor market, the two surveys tell roughly the same story over time. Month-to-month divergences are normal. But sustained divergence — the household survey consistently painting a darker picture than the establishment survey — is a warning signal that experienced labor market analysts take seriously.

The household survey has now shown a loss of employment in every single month of 2026. January, February, March, April — four consecutive months of household survey employment declines. The establishment survey has shown gains in every month except February.

Four consecutive months of divergence in the same direction is not statistical noise. It is a pattern. And the pattern says: the people being surveyed are telling the BLS they don’t have jobs at the same time that the businesses being surveyed are telling the BLS they have workers on payroll.

The 3-Month Average That Changes Everything

When the April headline of +115,000 is announced, it will be compared to the prior month’s +185,000 (March, after upward revision). The month-over-month comparison looks fine. Slower, but positive.

But the three-month rolling average — which smooths out the extraordinary month-to-month volatility that has characterized 2026 labor data — tells a completely different story.

Revisions pulled down the three-month average for job gains to 48,000 per month.

48,000 per month. That is the actual pace of job creation in the United States, averaged across the past three months including today’s revisions.

For context: economists estimate that approximately 100,000-120,000 new jobs per month are needed to absorb new labor force entrants and keep the unemployment rate stable — given current labor force growth constraints from demographics and immigration policy. A three-month average of 48,000 is less than half the breakeven rate.

An economy creating jobs at less than half the rate needed to keep pace with labor force growth should, in theory, be producing a rising unemployment rate. The unemployment rate is not rising — it is holding at 4.3%.

Why? Because the labor force is shrinking. People are leaving. They are not being counted as unemployed because they have stopped looking for work. And when people stop looking for work, they fall out of the unemployment calculation entirely.

This is the most important number in today’s report that is receiving almost no attention.

The labor force participation rate has declined from 62.6 to 61.8 percent. The labor force — the total number of people either employed or actively looking for work — has declined by more than 1 million. And the number of people employed has declined by more than 1.2 million.

The labor force shrank by over a million people. The number of employed people fell by over 1.2 million. These are the household survey numbers. They describe an America where people are not losing their jobs in mass layoffs — they are quietly leaving the workforce entirely.

The Real Unemployment Rate: 8.2%

The headline unemployment rate is 4.3%. That number gets the attention, the graphic, the anchor’s commentary.

But the BLS produces a second, broader unemployment measure every month — the U-6. It is not hidden. It is published in the same report. It includes, in addition to the officially unemployed, two additional groups that the headline rate excludes: marginally attached workers (people who want jobs and have looked in the past year but not in the past four weeks) and people working part-time for economic reasons (people who want full-time jobs but can only find part-time work).

The U-6 measure, now at 8.2%, captures some of this shift in individuals leaving the labor force.

8.2% is the real unemployment rate. The one that counts the people who have given up looking. The one that counts the people who took a part-time job because they couldn’t find a full-time one.

That is two full percentage points above what we saw in 2019.

In 2019, the labor market was considered historically strong. Economists were using phrases like “the best job market in 50 years.” U-6 was around 6.2%.

Today, with the headline unemployment rate matching 2019 levels (4.3%), the U-6 is two full percentage points higher. That gap — between the headline rate and the broader reality — represents millions of Americans who are counted as “not unemployed” but are clearly not experiencing the labor market conditions that the headline number implies.

Those who were forced to accept part- instead of full-time work rose by 445,000 in April alone.

445,000 Americans moved from full-time employment to involuntary part-time in a single month. These are workers who did not lose their jobs in the technical sense — they are still employed, still counted in the headline 115,000 — but whose income, hours, and economic security deteriorated significantly.

The AI Job Destruction Nobody Is Naming Directly

Buried in the sector breakdown of today’s report is a data point that should be generating considerably more discussion than it is.

Information services lost 13,000 jobs in April, part of a continuing trend that has seen the category down 342,000 jobs since November 2022, coinciding with the rise of artificial intelligence.

342,000 jobs lost in information services since November 2022. The timing is not ambiguous — November 2022 is when ChatGPT launched and the generative AI era began in earnest. The information services sector, which includes software publishing, data processing, and other technology-adjacent roles that are most directly exposed to AI substitution, has lost 342,000 jobs in the same period that the largest technology companies in the world have been deploying AI across their operations.

These are not manufacturing jobs, not retail jobs, not hospitality jobs. These are white-collar, knowledge-economy jobs — the category that was supposed to be safe from automation, that was supposed to benefit from AI as an assistive tool rather than being replaced by it.

342,000 jobs in one sector. Over 30 months. At an accelerating pace.

The White Collar Bloodbath post in this series, published in March, documented the wave of AI-driven layoffs at McKinsey, Salesforce, Microsoft, Nvidia, and other major employers. Today’s BLS data is the first official government confirmation that the pattern is real and is showing up in aggregate employment statistics.

Information services employment down 342,000 since AI launch. Not a forecast. An official government measurement.

Who Is Actually Leaving the Labor Force

The labor force participation rate fell to 61.8% in April — the lowest since October 2021. More than 1 million people left the labor force in a year. The question of who is leaving is as important as the fact that they are leaving.

Men over the age of 55 and prime age women — those 25 to 54 — accounted for the losses.

Two distinct groups. Two entirely different reasons.

Men over 55: Early retirement, voluntary and involuntary. In a labor market where knowledge-economy jobs are being eliminated by AI and knowledge-economy workers over 55 face significant age discrimination in re-employment, the choice between continued job searching and early retirement is not always voluntary. Many of the men leaving the labor force are not choosing leisure — they are accepting that re-employment at comparable compensation is unlikely and taking the Social Security and pension income available to them.

Prime age women (25-54): The childcare and return-to-office collision.

Prime age women with a bachelor’s degree or higher and small children at home have been dropping out of the labor force entirely in response to the high costs of childcare and return-to-office mandates.

This is one of the most consequential economic trends in the current data — and it is almost entirely invisible in the headline number.

Childcare costs have risen to the point where the math of working full-time while paying for childcare is, for many families, negative. A family with two young children in a major metropolitan area can face childcare costs of $3,000-4,000 per month. For a parent earning $60,000-75,000 annually, the post-tax income net of childcare is close to zero — or actually negative after commuting and other work-related costs.

Simultaneously, the return-to-office mandates that major employers have implemented in 2025-2026 have eliminated the flexibility that made dual-income households with young children mathematically viable. Remote work allowed a parent to be geographically available during school pickup windows, sick days, and school closures without burning vacation time. The elimination of remote flexibility, in a world of $3,000-4,000 monthly childcare costs, is pushing prime-age women out of the workforce in a pattern that the April data makes visible.

The eldercare market is in crisis. Men make up almost half of all unpaid elder care providers.

The men over 55 who are leaving the labor force are not only retiring. Many are becoming unpaid caregivers for aging parents in a healthcare system where professional elder care is increasingly unaffordable. This is the hidden demographic crisis inside the labor force participation rate.

Federal Employment: Down 348,000 From Peak

Federal employment is now down 348,000 jobs from its peak in October 2024. Staffing shortages have become acute at some federal agencies; older workers took buyouts, early retirement and quit in the wake of last year’s cuts.

348,000 federal jobs eliminated since October 2024. This is the DOGE effect made numerical and official.

The cuts are not evenly distributed. They are concentrated in regulatory agencies, research institutions, social service administration, and the federal workforce that implements programs — not the military or law enforcement functions that have been protected or expanded.

The consequences of this concentration are beginning to show up in ways that the employment statistic doesn’t capture. Staffing shortages at the Social Security Administration affect processing times for disability and retirement claims. Shortages at the Veterans Administration affect service delivery to veterans. Shortages at the FDA affect drug approval timelines — the same FDA that is simultaneously being asked to certify new US pharmaceutical manufacturing facilities in the context of the pharmaceutical tariff transition.

The 348,000 federal job losses are in the headline establishment survey. They are one reason the overall headline looks worse than it might otherwise — federal employment has been a persistent drag on an otherwise positive private sector picture.

But the economic impact of those 348,000 jobs extends well beyond the employment statistic. The services those workers provided don’t stop being needed just because the workers are gone.

The Housing Market Signal Hidden in Plain Sight

The residential building construction sector lost 1,500 jobs and residential specialty trade contractors shed 8,900 positions. Real estate also lost jobs in April, with employment falling by 1,700 jobs, while rental and leasing services employment fell by 3,600 jobs.

These are small numbers relative to the 115,000 headline. But they are directionally significant.

Residential construction employment falling — in a month that should be seeing seasonal strength as spring building season begins — signals that homebuilders are pulling back on activity. With mortgage rates at 6.75-7%, the economic math of homebuilding has deteriorated. Builders who started projects at lower rates are completing them. New project starts are declining.

Real estate employment falling — agents, brokers, property managers — reflects the transaction volume collapse that accompanies high mortgage rates. Fewer transactions mean less commission income, which means fewer employed real estate professionals. The housing market contraction that the MBA has been documenting for months is now showing up in employment data.

The Fed’s “higher for longer” policy, maintained to fight the inflation that the Iran war has re-accelerated, is producing a housing market contraction that is measurable in construction and real estate employment. The homebuyer who is waiting for rates to fall is waiting for a Fed that cannot cut. And the workers who depend on housing market activity are feeling the consequences.

What The Numbers Together Actually Say

The April 2026 jobs report, read in full, says this:

The establishment survey shows 115,000 new hires — employers adding workers to payrolls at a rate better than consensus, concentrated in healthcare, transportation, and retail.

The household survey shows 226,000 fewer employed people — workers reporting to surveyors that they don’t have jobs, even as employers report them on payrolls.

The labor force shrank by over a million people over the past year. The people leaving are not being counted as unemployed. The unemployment rate holds at 4.3% not because the labor market is strong but because the denominator — the number of people looking for work — is falling.

The U-6 “real” unemployment rate is 8.2%. Two percentage points above 2019. 445,000 Americans moved from full-time to involuntary part-time in April alone.

Information services has lost 342,000 jobs since AI launched in November 2022. Federal employment is down 348,000 from its October 2024 peak. Residential construction and real estate shed jobs in what should be the spring building season.

The three-month average payroll gain — after today’s revisions — is 48,000. Less than half the breakeven rate.

This is the jobs report that the headline number is not describing. Both are true. The 115,000 is real. The rest of this is also real.

The question is which truth more accurately describes the economic experience of the 160 million Americans in the labor force.

The consumer confidence data — at a 75-year low — suggests they have already voted on that question.

This is not financial advice. Always consult a qualified financial advisor before making significant financial decisions. If this gave you a clearer picture of what was actually inside this morning’s jobs report beyond the headline — share it with someone who heard “115,000” and thought the economy was fine. And subscribe below for the next one.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

- where your money is leaking,

- what to cut or renegotiate first,

- how to protect your savings,

- and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

>Get The $1,000 Money Recovery Checklist<

Leave a comment