The White Collar Job Collapse of 2026: What Your Boss Isn’t Telling You

Layoffs are accelerating in March 2026 — and it’s not the economy. It’s something far more permanent. Here’s what’s really happening, who’s getting rich from it, and how to protect yourself before it’s too late.

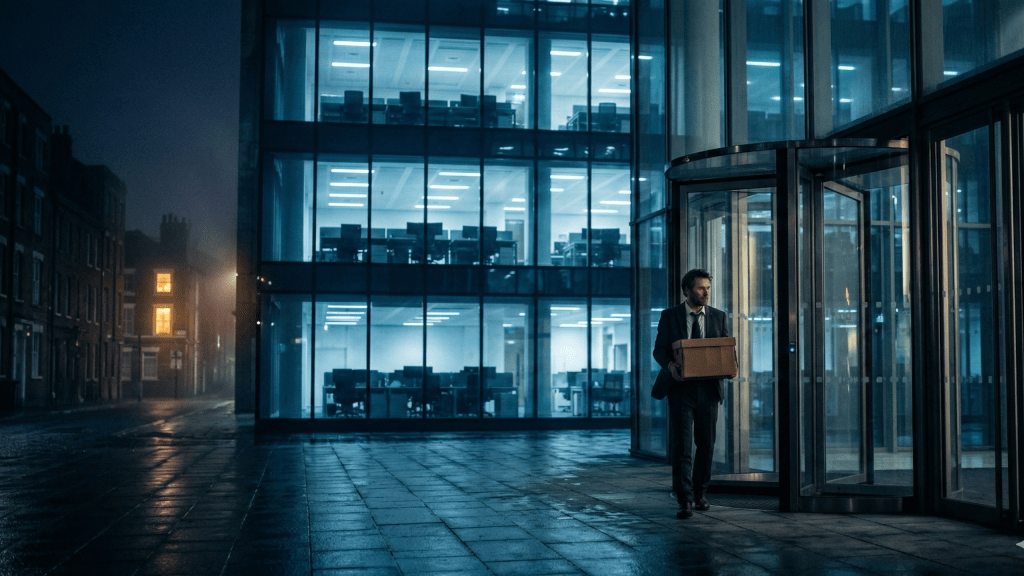

The memo went out on a Tuesday morning in February 2026.

No warning. No performance review. Just a calendar invite titled “Important Company Update” — and by 2pm, 340 people who had spent years building careers in finance, marketing, legal, and operations were clearing out their desks.

This wasn’t a struggling startup. This was a Fortune 500 company. And this wasn’t a cost-cutting move driven by a bad quarter.

It was something far more permanent.

The CEO said it publicly in the earnings call the following week: “AI agents have now taken over functions that previously required entire departments.” The stock went up 14% that day.

The employees? They’re still refreshing LinkedIn.

This is the story of March 2026 — and it’s only getting louder.

This Isn’t a Recession. It’s Something Worse.

Here’s the critical distinction most people are missing right now:

When recessions hit, jobs disappear temporarily. Companies pull back, weather the storm, and eventually rehire. The playbook is brutal but familiar — polish the resume, network aggressively, wait it out.

What’s happening in 2026 is categorically different. The jobs aren’t paused. They’re eliminated. And they are not coming back — not in the same form, not at the same volume, not at the same pay grade.

McKinsey’s March 2026 labor report landed like a bomb inside corporate HR departments: across knowledge work industries, AI agents are now performing at or above mid-level human employee output in 67% of measured task categories. That number was 31% just eighteen months ago.

The doubling happened faster than even the most aggressive forecasts predicted.

And the industries getting hit hardest right now — in Q1 2026 — are the ones that felt the safest just three years ago.

The Jobs Disappearing Fastest Right Now (March 2026)

Let’s be direct. The data is clear and it’s accelerating.

Financial Analysis and Reporting Automated financial modeling, variance analysis, and earnings reporting that once required teams of analysts is now handled by AI systems at a fraction of the cost. Goldman Sachs, JPMorgan, and dozens of mid-size asset managers have quietly reduced junior analyst headcount by 30–60% since 2024. The survivors are the ones who can ask better questions — not the ones who can build the spreadsheet.

Paralegal and Legal Research AI legal research tools are now producing case research in minutes that previously took paralegals days. Major law firms are not renewing paralegal contracts at renewal rates. First-year associate billing hours are down across AmLaw 100 firms. The legal profession is not disappearing — but its support infrastructure is hollowing out fast.

Mid-Level Marketing and Content Roles The CMO still exists. The VP of Brand still exists. But the coordinator, the copywriter, the junior content strategist, the SEO specialist running routine tasks — these roles have been quietly restructured across thousands of companies since late 2025. Marketing departments that had 12 people now run effectively with 4.

Customer Success and Operations Roles AI agents now handle tier-1 and tier-2 customer support, onboarding workflows, and routine account management with higher consistency scores than their human predecessors. Companies report cost reductions of 70–80% in these functions. Entire departments are being replaced by a product subscription and one human manager overseeing the AI.

Data Entry, Reporting, and Administrative Work This one should surprise no one — and yet thousands of people who held these roles through 2024 expected it to somehow pass them by. It hasn’t.

What Your Boss Actually Knows (And Isn’t Saying)

If you work in one of these industries, here’s what’s happening in boardrooms and executive offsites right now:

Leadership teams are sitting on workforce reduction roadmaps that span 12 to 36 months. These aren’t reactive decisions made in a bad quarter — they’re strategic plans with timelines, milestones, and budget reallocations already modeled out.

The reason they’re not announcing it: severance liability, talent retention during transitions, and PR optics. The playbook is to let attrition do most of the work — don’t replace the people who leave — while deploying AI into the functions quietly, role by role.

By the time the announcement comes — if it comes at all — the restructuring is already 80% complete.

You will not receive advance notice. That is the design.

The Counterintuitive Truth: This Is Creating Enormous Wealth

Now here’s where the narrative shifts — because if this article is only about fear, it’s not useful to you.

Every major labor disruption in history has created two groups: those who lost ground and those who gained it. The Industrial Revolution impoverished handloom weavers and created factory owners, railroad barons, and an entirely new middle class in a single generation.

The AI disruption of 2026 is no different. While 340 people cleared out their desks at that Fortune 500 company, four people at a competitor — a two-year-old startup with 11 employees — just closed a $40 million Series A round. Their product? An AI agent platform for exactly the workflow the Fortune 500 just automated.

The wealth is not disappearing. It is moving.

And here’s who’s capturing it right now:

The 5 Profiles Getting Rich in the Q1 2026 Job Market

The AI Workflow Architects These are the people — often former operations or project management professionals — who learned how to design, deploy, and manage AI agent workflows inside companies. They are not coders. They are systems thinkers who learned a new toolset. Enterprise demand for this skill set is currently outpacing supply by a significant margin. Compensation packages for senior AI Workflow Architects at mid-market companies now routinely exceed $180,000 base.

The Niche Educators The single biggest bottleneck in the AI economy right now is not technology — it’s adoption. Millions of professionals know they need to adapt and have no idea how. The people who are teaching specific, practical AI skills to specific professional audiences — accountants, therapists, real estate agents, HR professionals — are building course businesses, coaching practices, and membership communities that are scaling fast. The niche educator who owns a specific professional audience right now has one of the most valuable positions in the 2026 economy.

The Human-In-The-Loop Specialists AI makes a lot of decisions well. It makes some decisions catastrophically wrong. Companies deploying AI at scale are discovering they need highly skilled humans to audit, correct, and refine AI outputs in high-stakes domains — medical, legal, financial, regulatory. These roles pay a premium precisely because the human judgment they require cannot be automated away. Radiologists who work with AI diagnostic tools are billing more than they ever did before. The same pattern is appearing in law, finance, and engineering.

The Micro-Business Operators The cost of starting and operating a small business has collapsed in 2026. A solo operator with the right AI stack can now deliver services that previously required a 10-person agency. Design, copywriting, financial analysis, customer service, appointment scheduling, social media management — all of it can be AI-assisted, allowing one person to serve dozens of clients simultaneously. The micro-business boom of 2026 is quietly producing a new class of six-figure solopreneurs that official employment statistics aren’t capturing.

The Attention Landlords In an economy flooded with AI-generated content, the scarcest resource is not content — it’s trusted attention. The people who have built audiences — newsletters, YouTube channels, podcasts, LinkedIn followings, niche communities — are sitting on the most valuable real estate in the 2026 economy. Advertisers, brands, course creators, and software companies are paying significant premiums to reach engaged, loyal audiences. If you don’t have an audience yet, you should be building one now. This window will not stay open indefinitely.

The Three Moves That Separate Who Wins from Who Waits

There is no perfect playbook. But right now, in March 2026, there are three decisions that appear consistently in the trajectories of people who are thriving versus those who are struggling.

Move 1: Stop Waiting for Certainty The people winning in 2026 started moving before they had complete information. They picked a direction — a new skill, a niche, a business model — and committed. The people waiting for certainty are discovering that certainty in a disrupted market arrives approximately six months too late to be useful.

Move 2: Convert Your Existing Expertise Into Leverage The fastest path to income in the AI economy is not starting from zero — it’s taking the domain expertise you already have and layering AI capability on top of it. A 15-year marketing veteran who masters AI marketing tools doesn’t become obsolete — she becomes a one-person agency that can outperform teams three times her size. Your existing knowledge is the moat. AI is the amplifier.

Move 3: Build Something You Own Salaries are what companies pay you to build their assets. In 2026, with job security at its lowest point in a generation, the asymmetric bet is to simultaneously build something you own — an audience, a product, a recurring revenue stream, a scalable skill — that exists independently of any employer’s quarterly decisions. You don’t need to quit your job to do this. You need to start.

The Question You Need to Sit With

By the end of 2026, the labor economists broadly agree on one thing: the knowledge economy will look fundamentally different than it does today. Not slightly different. Fundamentally.

Some people will look back on March 2026 as the month they finally started paying attention. They’ll remember the exact article, the exact conversation, the exact moment something clicked — and they decided to move.

Others will look back on March 2026 as the month they kept waiting.

There is no neutral position here. Standing still in a moving current is still a choice — it just doesn’t feel like one until the water’s over your head.

The question isn’t whether AI is reshaping the economy. That is settled. The question is whether you are reshaping yourself fast enough to stay ahead of it.

What are you going to do differently this week?

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

- where your money is leaking,

- what to cut or renegotiate first,

- how to protect your savings,

- and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

>Get The $1,000 Money Recovery Checklist<

Found this valuable? Share it with someone who needs to hear it right now — they might thank you for it later. And subscribe below to get the next piece before the rest of the internet does.

white collar jobs 2026, AI layoffs, job market 2026, AI economy, future of work, how to make money 2026, career change AI, passive income 2026, AI disruption

Personal Finance / Future of Work