Most people hear “$200 oil” and think: that’s an abstract Wall Street number. Something that happens on a Bloomberg terminal. Something for traders.

It isn’t.

$200 oil is a grocery bill. It’s a mortgage payment you can’t make. It’s an airline ticket that costs as much as a car payment. It’s a small business that can’t afford to deliver its product. It’s a retirement account that stops growing because the economy has ground to a halt.

And it is no longer a theoretical scenario.

Wood Mackenzie analysts said last week that Brent could hit $150 soon, and that $200 was not “outside the realms of possibility” in 2026. Iran’s own military spokesperson warned the world to “get ready” for such a spike. TD Securities published a research note last week saying oil could eventually top $200 a barrel if the conflict drags on.

As of yesterday morning, Brent crude sat at $99.75 per barrel — $26.64 more than at this time last year. Today it pushed back above $108 as Iran formally rejected the American peace proposal and Israeli strikes continued.

The five-day pause that briefly gave markets hope on Monday is already fraying. The scenario that institutional analysts are being paid to model — $200 oil — is not a tail risk anymore. It’s a live scenario with a meaningful probability.

Here is exactly what that number means for your actual life. Not for portfolios. Not for trading desks. For you.

How We Get From $108 to $200

Before the numbers, the mechanism. Because understanding how $200 happens changes how you respond to it.

The Strait of Hormuz crisis has already caused the biggest oil supply disruption in history. Brent futures nearly touched $120 per barrel as tanker traffic through the Strait effectively ceased. The IEA’s March 2026 oil market report confirms that oil prices have gyrated wildly since the US and Israel launched joint airstrikes on Iran on February 28.

The global oil market operates with a razor-thin spare capacity buffer of merely 2% to 3% above daily consumption requirements. When 8% of global energy supply is abruptly removed from the market due to hostilities, the economic consequences compound rapidly.

The mathematical path to $200 requires no dramatic escalation from here. It requires only that the Strait of Hormuz remains effectively closed for 60 to 90 days. That is all. No nuclear exchange. No ground invasion. Just the continued absence of tanker traffic through a 21-mile strait.

The IEA noted that even with an unprecedented 400 million barrel emergency reserve release agreed to by member countries on March 11, this remains a stop-gap measure — in the absence of a swift conflict resolution, it cannot bridge a sustained disruption.

If talks collapse this week — and Iran’s rejection of the American proposal today suggests that is the more likely outcome — the world finds out what sustained disruption looks like.

Your Gas Tank: The Most Immediate Impact

The national average gasoline price reached $3.79 a gallon as of last Tuesday — up about 87 cents per gallon, or 30%, from a month ago, according to AAA.

Oil at $100 already brings $5 gas — we saw exactly that pattern in 2022 after the Ukraine war began, when CPI hit 9.1% in June of that year.

At $150 oil, analysts project gasoline at $6.50 to $7 nationally — with California and other high-tax states approaching $8 to $9 per gallon.

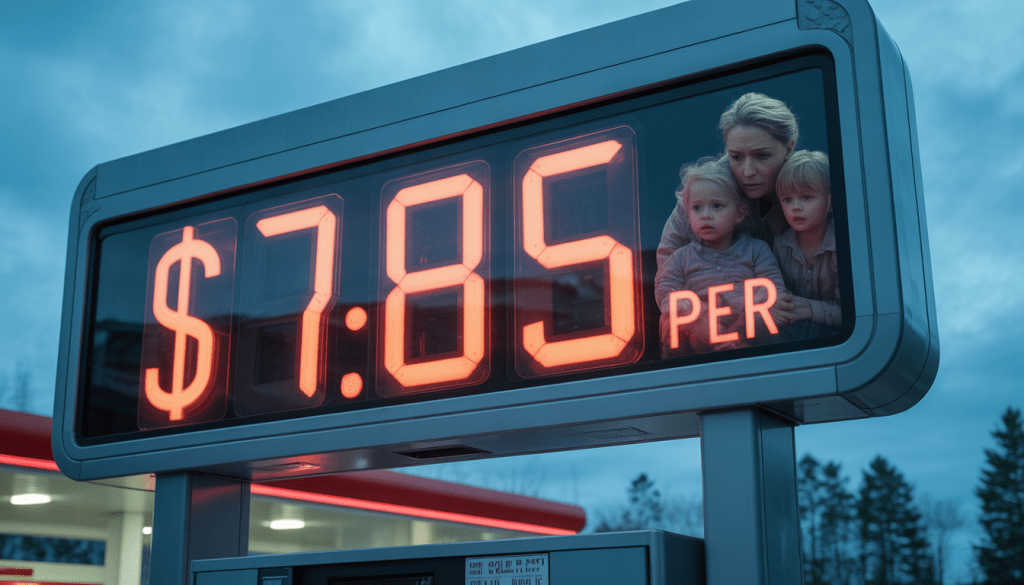

At $200 oil, the estimated national average gasoline price hits $7.85 per gallon.

For the average American who drives 15,000 miles per year in a vehicle getting 28 miles per gallon: that’s roughly 535 gallons annually. At $7.85 per gallon, your annual gasoline cost exceeds $4,200 — an increase of approximately $2,100 per year compared to where prices were twelve months ago. That is $175 per month in additional gasoline spending alone, for a family that hasn’t changed a single driving habit.

For families with two vehicles, two commutes, and children in activities: the math is worse.

Your Grocery Bill: The Impact Nobody Sees Coming

US diesel prices have already topped $5 per gallon for the first time since 2022. That drives up trucking costs, which push up the prices of food and other goods. Volatile oil prices have a knock-on effect, driving prices higher across the entire economy, experts said.

Here is the mechanism most people don’t understand: oil doesn’t just power cars. It powers the entire agricultural and food supply chain.

Farm equipment runs on diesel. Fertilizer is manufactured from natural gas — and natural gas prices are directly linked to oil prices. Irrigation pumps run on electricity generated partly from fossil fuels. Refrigerated trucks that move food from farms to distribution centers run on diesel. The ships that import food run on fuel oil. The planes that carry perishables run on jet fuel.

Historical data is unambiguous: large and sustained oil price movements have historically coincided with changes in both food prices and broader consumer inflation. In 2022, when Brent crude surged above $120 per barrel following Russia’s invasion of Ukraine, the Global Food Price Index reached its highest level on record and world inflation rose sharply.

Pantheon Macroeconomics found that if oil prices increase to $150 per barrel and stay at that level for three months, the Consumer Price Index could jump to an annual pace of 6%, up from 2.4% recorded in February. At $200 sustained, economic modeling suggests CPI acceleration toward double digits is plausible — and the immediate macroeconomic implication is the onset of virulent stagflation: a paralyzing combination of contracting economic growth and surging consumer prices.

For a family spending $1,200 per month on groceries today: a 15% food price increase adds $180 per month to the grocery bill. A 25% increase — well within historical range for a sustained oil shock — adds $300 per month. Combined with the gasoline impact, a household can find itself spending $500 to $600 more per month on necessities alone, without changing a single behavior.

Your Utility Bills: The Invisible Multiplier

Electricity generation in the United States still depends significantly on natural gas — and natural gas prices move with oil. When oil spikes, so do electricity generation costs, and those costs flow through to your monthly utility bill with a lag of approximately 60 to 90 days.

The households that will feel this most acutely are the ones already in energy-stressed situations: families in the American South and Southwest where air conditioning is not optional, rural households dependent on heating oil for winter warmth, and working-class families in older housing stock with poor insulation who cannot afford the upgrades that would reduce their energy consumption.

Stanford economics professor Nicholas Bloom said he worries that rising oil and gasoline prices fuel the economy’s K shape — higher-income households do better and better while lower-income households fall further behind. “That, I think, is a major concern as an economist: inequality,” Bloom said during a Harvard Kennedy School webinar on the economic consequences of the Iran war.

The K-shaped economy doesn’t begin with $200 oil. It accelerates with it.

Your Flights and Travel: When the Number Hits $200

Global prices for jet fuel — a major cost component for airlines — are already up approximately 83% over the past month, according to International Air Transport Association data.

Airlines do not absorb fuel cost increases indefinitely. They pass them through as fuel surcharges, higher base fares, and reduced route options for markets that become unprofitable to serve.

At $200 oil, domestic round-trip airfares are projected to increase by $150 to $300 per ticket for most markets. International fares see larger increases. Budget carriers — the airlines that made flying accessible to families who couldn’t afford legacy carrier pricing — face existential pressure, as their model depends on volume at thin margins that evaporate when fuel costs double.

The family vacation that was budget-stretched at $3,000 in a normal year becomes genuinely inaccessible at $4,500 in a $200 oil world.

Your Job and Business: The Downstream Damage

An Oxford energy expert told Al Jazeera that $200 oil “would be a major handbrake to the world economy,” describing the prospect as “perfectly possible,” and warned it would “impact inflation, growth, employment and in some cases cause shortages of not just fuel but also materials such as fertilisers, plastics and the like.”

Plunging LPG and naphtha supplies are already forcing petrochemical plants to curb production of polymers — creating shortages of materials that flow into everything from food packaging to medical devices to construction materials.

The businesses most vulnerable are not large corporations with hedging programs and balance sheet depth. They are the small businesses — the restaurant that can’t absorb a 30% increase in food delivery costs, the landscaper whose fuel bill doubled, the small manufacturer whose plastic input costs spiked, the regional trucking company running on thin margins that evaporated when diesel crossed $5.

Ramnivas Mundada of GlobalData noted: “Even if oil prices stabilize, the persistence of higher freight costs, longer shipping routes, and insurance costs can keep delivered prices elevated for fuel and intermediate goods — and that combination increases the likelihood that inflation proves stickier than expected.”

Sticky inflation means the Fed stays hawkish longer. The Fed staying hawkish longer means rates stay elevated. Rates staying elevated means the small business loan that was already expensive becomes prohibitive. The commercial real estate refinancing that was already painful becomes impossible. The mortgage modification that was already difficult becomes a conversation that ends badly.

The cascade from $200 oil to your specific job or business depends entirely on where you sit in the supply chain — but almost nobody sits outside it.

The Scenarios Wall Street Is Actually Modeling

The institutional investment community is not operating on hope right now. It is operating on scenario trees — branching probability-weighted outcomes that determine position sizing and hedging strategies.

The three scenarios that appear most frequently in the research notes circulating among serious macro investors this week are:

Scenario One — Negotiated Resolution (30-day timeline): Talks succeed, Hormuz partially reopens, Brent falls toward $75-85, CPI moderates. This scenario is assigned roughly 30% probability by most models — reduced from 50% after Iran’s rejection of the American proposal today. In this scenario, the gas price pain is real but temporary, and the economic damage is significant but manageable.

Scenario Two — Prolonged Partial Disruption (3-6 months): The conflict continues at current intensity, Hormuz remains effectively closed, emergency reserves bridge partial supply gaps, Brent oscillates between $100 and $140. CPI settles in the 5-7% range. The Fed cannot cut rates. Small business failures accelerate. The K-shaped economy deepens. This scenario is assigned roughly 50% probability by most models.

Scenario Three — Escalation to $200 (triggered by Iranian infrastructure strikes or Gulf-wide expansion): Israeli strikes on Kharg Island or other Iranian export infrastructure, or Iranian mining of the broader Persian Gulf, triggers the supply shock that takes Brent to $150-200. CPI surges toward double digits. The Fed faces an impossible choice. Demand destruction begins — consumers reduce driving, defer purchases, cut discretionary spending. Recession probability crosses 60%. This scenario is assigned 15-20% probability — low enough to feel manageable, high enough that every serious portfolio manager has a hedge in place.

The One Number That Changes Everything Else

Here is the thing about $200 oil that the Wall Street scenario models capture mathematically but don’t fully convey humanly:

It is not a price. It is a reorganization of economic life.

At $200 oil, the decisions that seemed like personal choices — where you live relative to your job, what kind of car you drive, how often you fly, where you shop for groceries — become financial necessities or impossibilities. The optional becomes mandatory. The possible becomes unaffordable.

The households that made decisions in a $50 oil world — long commutes, large vehicles, houses far from urban centers where land was cheap — are the most exposed. Not because they made bad decisions. Because the world changed around them.

The businesses that built supply chains optimized for cheap transportation — goods manufactured far away and shipped cheaply — face a cost structure that their pricing cannot absorb.

The government faces a Fed that cannot cut rates and a consumer that cannot spend and a budget that has no room for stimulus and an energy system that has no quick fix.

Applying Blanch’s macroeconomic rule of thumb: every 1% of energy lost equates to a 1% contraction in global GDP. An 8% supply disruption implies a potential 8% shock to global economic output.

That is not a recession. That is a depression-level supply shock.

What You Can Actually Do Right Now

This post is not meant to induce panic. Panic is the response that serves you least in exactly these circumstances. But information — real, specific, uncomfortable information — is what allows you to make decisions that matter.

Here is what is actionable right now, in March 2026, while the scenario is still unresolved.

Reduce your fuel exposure now, not if prices spike further. Consolidate trips. Work from home where possible. Carpool. These are not dramatic measures — they are rational adjustments to a price signal that is already telling you something real.

Audit your variable costs. The expenses that scale with inflation — food, fuel, utilities, services — are the ones to optimize right now, before the full pass-through arrives in your bills. Pantry stocking at current prices, locking in utility rate plans where available, reviewing subscriptions and discretionary spending: boring, practical, effective.

Build your cash cushion now. High-yield savings accounts are paying 4-5% and that rate will persist in a higher-for-longer rate environment. Three to six months of expenses in liquid cash — at current inflation levels, that means a higher nominal amount than your previous emergency fund target — is the single most powerful defensive financial move available to most people right now.

If you own a business, price the risk immediately. The businesses that survive supply shocks are the ones that repriced before they had to, not the ones that absorbed margin compression until it was too late. If your cost structure has meaningful fuel or food input exposure, your pricing conversation with customers needs to happen this week, not after the next bill arrives.

If you are invested in rate-sensitive assets: the scenario that allows the Fed to cut rates and provide relief to mortgage holders, bond investors, and growth stocks requires a resolution to the conflict that is not currently in sight. Position your portfolio for the scenario that is actually unfolding, not the one you were hoping for three months ago.

The World That Was, and the World That Is

Twelve months ago, the EIA was projecting Brent crude at $55 per barrel for 2026. Gas prices were expected to fall toward $3 per gallon nationally. The Iran conflict did not exist. The Strait of Hormuz was open. The scenario being modeled in institutional risk departments was deflation, not inflation.

That world is gone.

The world that exists today has oil at $108 and rising, a Strait that has been effectively closed for 26 days, a Fed that cannot cut rates, a consumer whose confidence just hit a historic low, and a military conflict with no clear resolution pathway.

As one analyst put it: “In several respects, the conditions today could allow for an even more dramatic move than the Gulf War, given the larger share of global supply potentially at risk and the wider imbalance between supply and demand.”

$200 oil is not inevitable. But it is no longer implausible. And the gap between implausible and happening has closed faster than almost anyone predicted over the past 26 days.

The question is not whether you believe it will happen.

The question is whether you’re prepared if it does.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

- where your money is leaking,

- what to cut or renegotiate first,

- how to protect your savings,

- and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

>Get The $1,000 Money Recovery Checklist<

This is not financial advice. Always consult a qualified financial advisor before making significant financial decisions. If this gave you a clearer picture of what $200 oil actually means for your life — share it with someone who needs to understand what’s at stake right now. And subscribe below for the next one.

Leave a comment